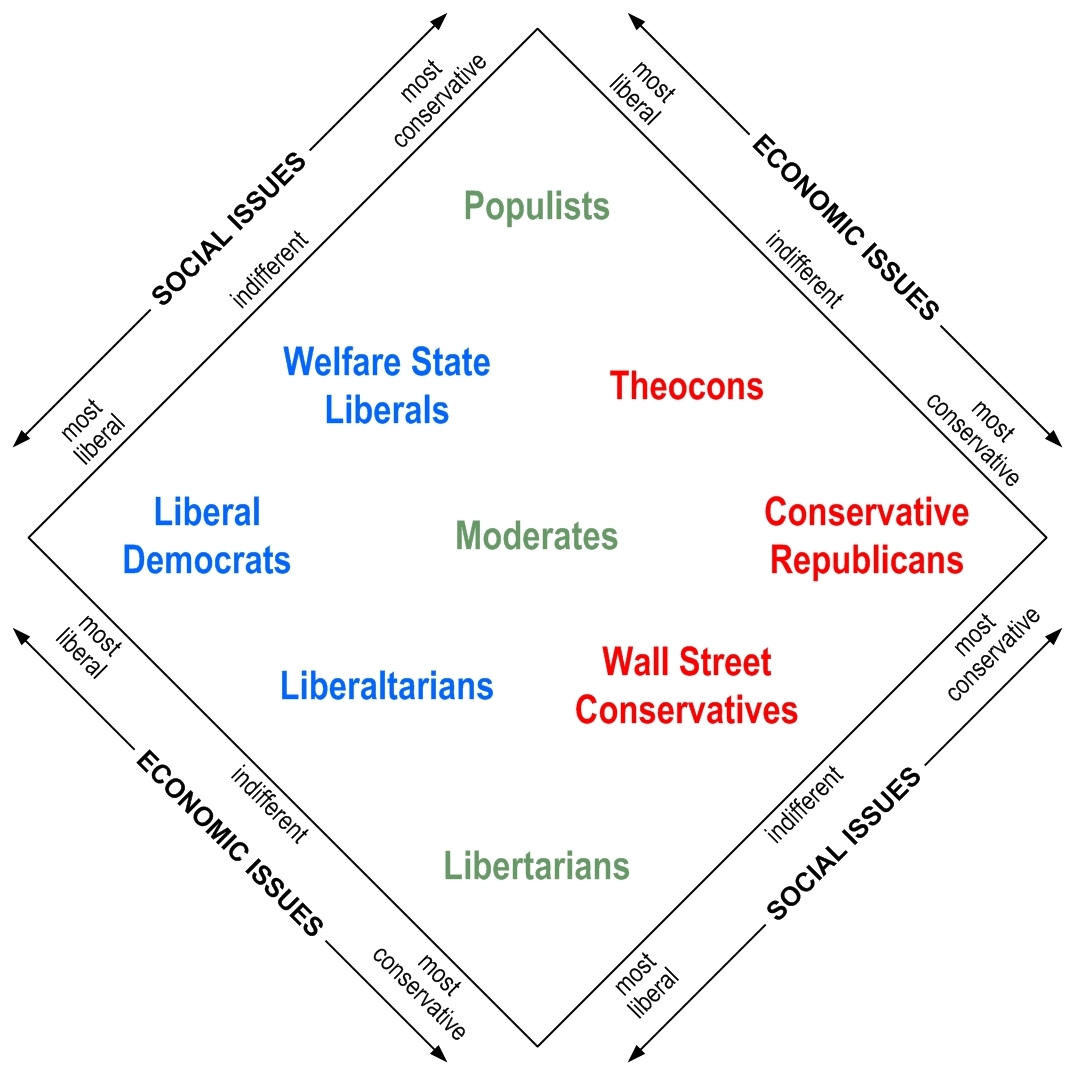

Biaxial incoherence in American politics, or, why the center cannot hold.

We will, in fact, be greeted as liberators.

Note to Cliff:

What exactly did you find so consequential or even provocative about this piece? It revolves around the assertion that no one loves Obama anymore, on the basis of conversations Noonan’s had. Uh huh. She didn’t ask me, that’s for sure. Reminds me of what Pauline Kael is supposed to have said after the 1972 elections: “Nixon? I can’t believe it. I don’t know anybody who voted for him.”

The other evidence Noonan marshals – the Obama campaign’s want ad for predictive modeling specialists – says more about her distrust of quantitative analysis, lest it affect her pre-determined conclusions, than it does about Obama’s humanity.

But the launching pad for this unscientific bit of mass psychology is even more meaningless. Let’s see if I have this right: the Tea Party movement and the Republican establishment, by joining in support of the Boehner proposal, have each succeeding in moderating the excesses of the other. Moderating? The Tea Party movement wants to use the debt limit increase as a vehicle for forcing deficit reductions that rely entirely on spending cuts, with no tax increases, even if this means driving the economy back into recession. The Republican establishment wants to destroy Obama’s presidency and ensure his defeat in 2012, even if this means driving the economy back into recession. With the Boehner proposal, the Tea Party gets what it wants, although maybe not everything its ideological heart desires, and the Republicans double-down on wreaking havoc with the economy as their only strategy for winning back the White House in 2012.

This path is neither Burkean nor viable and Noonan’s a loser for endorsing it. Boehner’s a loser for permitting it (although I like and feel for the guy, I really do), and the rest of us are just plain losers.

On November 19, 2010, the Securities and Exchange Commission (SEC) issued proposed rules relating to provisions of the Dodd-Frank Act that expand the SEC’s regulatory authority over investment advisers to include many more investment advisers to private equity and hedge funds, subject to certain exemptions.

Later, a non-U.S. investment adviser went to the SEC’s Division of Investment Management to get a Foreign Private Adviser Exemption, as described in the Dodd-Frank Act.

This is the story of that investment adviser.

You are a true believer. Blessings of the state. Blessings of the masses. Thou art a subject of the divine. Created in the image of man, by man, for man. Let us be thankful we have commerce. Buy more. Buy more now. Buy more and be happy.

Short of direct stimulus spending, a payroll tax holiday — at least with respect to the employee’s portion of Social Security and Medicare taxes — looks like the best, fastest and most politically feasible way to put money into the hands of people who will actually use it to buy more. A holiday on the employer’s portion of payroll taxes, albeit a necessary (if not sufficient) condition for Republican support, is going to be less effective stimulus. To the extent the employee’s portion gets spent, the increase in aggregate demand is likely to have a greater impact on hiring decisions than the reduction in employers’ cost per employee.

Let us be thankful we have an occupation to fill. Work hard, increase production, prevent accidents, and be happy.

Either way, of course, a tax cut that actually works to stimulate the economy is the last thing the Republicans want. Republican congressmen will accuse Obama of raiding the Social Security and Medicare trust funds so he can buy free lunches for illegal immigrants and build a mosque in your home town, and New York Post readers will believe. Republican advisors will argue that only regressive tax cuts create jobs, and Fox News Channel viewers will believe. Republican lobbyists will say that because a payroll tax holiday is only temporary, it results in more “regime uncertainty” and further undermines business confidence, and Wall Street Journal readers will believe. And all the true believers will know, on some level, that two more years of slow-or-no growth and high unemployment is the key to Republican hopes in 2012.

For more enjoyment and greater efficiency, consumption is being standardized.

Would a 1:1000 scale model of conservative aspirations look any more realistic than Paul Ryan’s roadmap?

What the income-inequality denialists and “politics of envy” critics don’t want to see: pre-tax income and wage data compiled by Thomas Piketty (Paris School of Economics/EHESS) and Emmanuel Saez (Department of Economics, UC Berkeley, Director, Center for Equitable Growth, 2009 John Bates Clark medal winner).

From which data we’ve created a few visual displays of income concentration among the top 1% of U.S. families (the “merely rich”), the top 0.1% of U.S. families (the “very rich”) and the top 0.01% of U.S. families (the “filthy rich”) from 1950 to 2007. Headlines for 2007:

The income shares of the merely, very and filthy rich in 2007 were all much, much larger than they were in 1950 — 12.82%, 4.39% and 1.22%, respectively. Compared to the previous secular peak for income concentration in the late 1920’s, the 2007 income share of the merely rich was just shy of the 23.94% record set in 1928. The 2007 income shares of the very and filthy rich, however, were well in excess of the previous highs (also set in 1928) of 11.54% and 5.02%, respectively.

If the increase from 1950 to 2007 in the income share of the merely rich was remarkable, the increase in the income share of the very rich was truly exceptional and, as for the filthy rich … un-fucking-believable:

Looked at another way, the increase from 1950 to 2007 in the share of U.S. family income going to the top 1% as a whole was mainly attributable to increases in the income shares going to the very and filthy rich:

The accelerating growth of income concentration within the top 1% is evidence of nothing less than the emergence, especially since the 1980s, of an income plutocracy in the United States: